AI-Driven Trade Meets Geopolitical Headwinds

WTO Outlook Flags Shift in Global Trade Dynamics

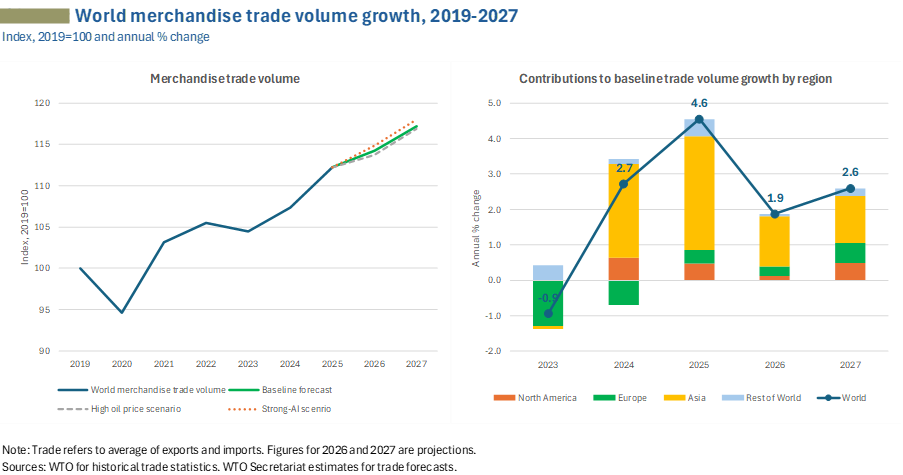

Geneva: Global trade is set to moderate in 2026 after a stronger-than-expected expansion in 2025, with the latest Global Trade Outlook and Statistics pointing to a transition from technology-driven acceleration to a more complex phase shaped by geopolitical tensions, shifting investment patterns and evolving macroeconomic conditions. The report, released on 19 March, projects that global merchandise trade volume growth will slow to 1.9% in 2026 from 4.6% in 2025, before recovering to 2.6% in 2027. Commercial services trade is expected to ease to 4.8% in 2026 and then strengthen to 5.1% in 2027, while overall trade in goods and services is forecast to grow by 2.7%, broadly in line with projected global GDP growth of 2.8%.

The deceleration follows a year in which trade outperformed expectations despite tariff pressures and policy uncertainty. In 2025, merchandise trade volumes rose 4.6%, supported by a surge in demand for AI-enabling goods and by policy-related factors that temporarily amplified flows. In value terms, global merchandise exports reached US$ 26.26 trillion, up 7% year-on-year, while services trade rose 8% to US$ 9.56 trillion, taking total global trade to US$ 34.65 trillion. This divergence between value and volume growth reflected strong price effects in some sectors and declining prices in others, with fuel trade values falling despite stable volumes, and precious metals such as gold contributing to value gains.

A central feature of the 2025 expansion was the rapid growth of AI-related trade, which increased 21.9% in value to US$ 4.18 trillion and accounted for 42% of total merchandise trade growth. This reflected a broader shift in the composition of global investment, with spending on AI infrastructure, data centres and associated technologies rising sharply across regions. Such investment is significantly more import-intensive than traditional sectors, with an estimated import content of 70–90%, compared with much lower levels in areas such as construction. As a result, the expansion of AI-related investment has increased the trade intensity of global growth, strengthening the link between capital formation and cross-border flows.

At the same time, part of the strength observed in 2025 reflected temporary dynamics. Anticipation of new tariffs led to frontloading of imports, particularly in North America, where demand was concentrated in the early part of the year. This effect, combined with inventory accumulation, boosted annual trade figures but is not expected to be repeated in 2026, implying that part of the projected slowdown represents a normalisation of trade patterns rather than a broad-based contraction in demand.

The structure of global trade is also becoming more concentrated around key economies and sectors. China remained a major driver of export growth in 2025, contributing roughly 30% of the global increase, supported by expanding capacity and strong performance in technology-related sectors. In the United States, import demand showed a clear divergence, with contraction in many traditional categories offset by a 38.3% increase in imports of AI-related goods. This pattern underscores a growing bifurcation in global trade, in which high-technology supply chains play an increasingly dominant role relative to other sectors.

Sectoral data reinforce this shift in composition. Trade in office and telecommunications equipment rose by 19% in 2025, reflecting strong demand linked to digital infrastructure, while fuels declined by 10% in value terms and automotive trade remained broadly stagnant. Machinery and chemicals recorded moderate growth. Together, these trends point to a reweighting of global trade away from energy-intensive goods towards technology-driven categories, with implications for both exporters and importers as relative demand patterns evolve.

Looking ahead, the outlook for 2026 is increasingly influenced by geopolitical developments, particularly the ongoing conflict in the Middle East. The report identifies energy prices as the primary transmission channel through which the conflict could affect global trade. In a scenario where crude oil and liquefied natural gas prices remain elevated throughout the year, global GDP growth could be reduced by around 0.3 percentage points, while merchandise trade growth could fall to 1.4%. Net fuel-importing regions, including Europe and parts of Asia, would face the largest impact through higher production costs, reduced real incomes and weaker import demand, while energy exporters could experience offsetting gains.

The effects of the conflict extend beyond energy markets into agriculture and food systems. Disruptions in the Strait of Hormuz, a key route for both energy and fertilizer shipments, have constrained supplies of critical inputs such as urea and ammonia, on which major agricultural producers including India, Thailand and Brazil depend. Higher input costs and supply uncertainty may influence planting decisions, reduce fertiliser use and affect yields, with potential knock-on effects for global food prices and trade flows. At the same time, Gulf economies, which rely heavily on food imports, face increased costs as supply chains are rerouted.

Services trade reflects similar pressures, particularly in transport and travel. The Middle East’s role as a global transit hub means that disruptions have immediate effects on connectivity, with traffic through key routes sharply reduced and more than 40,000 flights cancelled. These developments have raised transport and insurance costs and curtailed mobility. Under an adjusted scenario, services trade growth could slow to 4.1% in 2026, with the impact concentrated in transport and travel segments, while digitally delivered services continue to show relative resilience and steady expansion.

Early indicators suggest that global trade entered 2026 with underlying momentum. Container throughput rose by 6.1% year-on-year in January, and export orders indices remained in expansionary territory, pointing to continued activity prior to the escalation of geopolitical risks. These signals indicate that the projected slowdown is closely tied to recent developments rather than a prolonged weakening trend.

Regional patterns reflect both cyclical adjustments and structural positioning. Asia is expected to lead trade growth in 2026, supported by its central role in manufacturing and technology supply chains, while Africa and South America are projected to record moderate gains. Europe’s performance is likely to remain subdued due to energy constraints, and North America’s import growth is expected to flatten as the effects of earlier frontloading unwind. The Middle East faces a dual dynamic, with reduced trade flows through its transport corridors offsetting gains linked to energy exports.

At the same time, participation in global trade continues to broaden. Least-developed countries recorded an 11% increase in exports in 2025, reaching US$ 309 billion and raising their share of global trade to 1.21%. While still modest, this growth highlights the role of developing economies in supporting overall trade expansion and underscores the distributional dimensions of global trade dynamics.

Trade policy conditions remain relatively stable despite recent volatility. The share of global trade conducted on a most-favoured-nation basis stood at 72% by early 2026, indicating that multilateral tariff frameworks continue to underpin most cross-border flows. Recent policy changes have largely involved adjustments in legal instruments rather than broad increases in tariff barriers, limiting the direct impact of policy on trade volumes.

Beyond immediate trade and energy dynamics, the report also points to broader macro-financial risks. Elevated global debt levels and the possibility of financial market corrections could affect investment and demand, introducing additional uncertainty into the trade outlook. Monetary policy responses to inflationary pressures linked to energy prices may further influence the trajectory of trade by shaping financing conditions and consumption patterns.

The outlook for 2026 is therefore defined by the interaction of cyclical and structural forces. On the cyclical side, the unwinding of frontloaded demand, the normalisation of post-pandemic travel and inventory adjustments are expected to moderate growth. On the structural side, the expansion of AI-related investment is reshaping the composition and intensity of global trade, while geopolitical tensions are altering supply chains, transport routes and cost structures.

The balance between these forces remains uncertain. Continued strength in AI-related investment could add up to 0.5 percentage points to merchandise trade growth, while sustained energy price pressures linked to geopolitical tensions could reduce it by a similar margin. The extent to which these opposing dynamics materialise simultaneously will determine whether global trade in 2026 follows the baseline trajectory or diverges from it.

Taken together, the projections suggest that global trade is not only slowing but also evolving, with changes in technology, geopolitics and macroeconomic conditions reshaping how and where trade growth occurs. Whether this period marks a temporary adjustment following an unusually strong year or the beginning of a more sustained recalibration will depend on the durability of the current investment cycle and the trajectory of geopolitical risks in the months ahead.

– global bihari bureau