Shipping Collapse Links Energy Shock to Food Risks

Fertiliser Disruption Raises Global Food Concerns

Geneva: A near-total collapse in shipping through the Strait of Hormuz is now spilling beyond energy markets into global food systems, with measurable increases in fertiliser prices signalling growing risks for agricultural production, supply chains and food security, according to an analysis released on March 30, 2026, by the United Nations Trade and Development (UNCTAD).

The ongoing conflict affecting the Strait of Hormuz region, including Iran and the Gulf states, is disrupting energy and fertiliser flows simultaneously, with measurable impacts on costs and mounting risks for food systems, trade and vulnerable economies. The disruption is increasingly linking energy markets to food systems, with growing implications for trade and development outcomes.

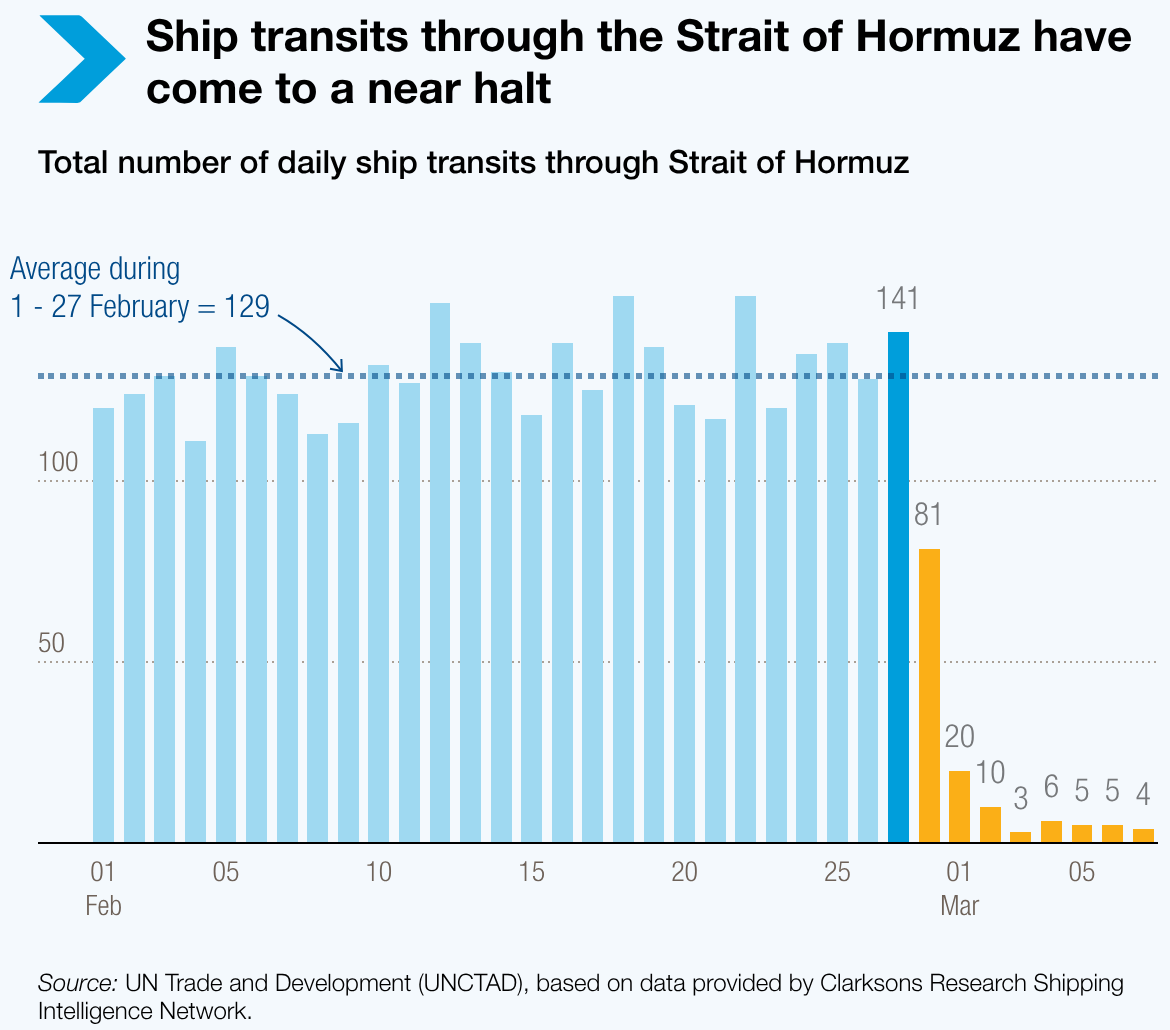

Shipping through the Strait has effectively collapsed, with vessel transits down by more than 95%. Data compiled by UNCTAD, based on Clarksons Research Shipping Intelligence Network, show that daily ship transits fell from an average of 103 vessels in the last week of February to single digits within weeks, bringing flows close to a standstill. Over the period from 1 to 27 February, average daily transits stood at 129 vessels, before dropping sharply to as low as three to six vessels per day in early March.

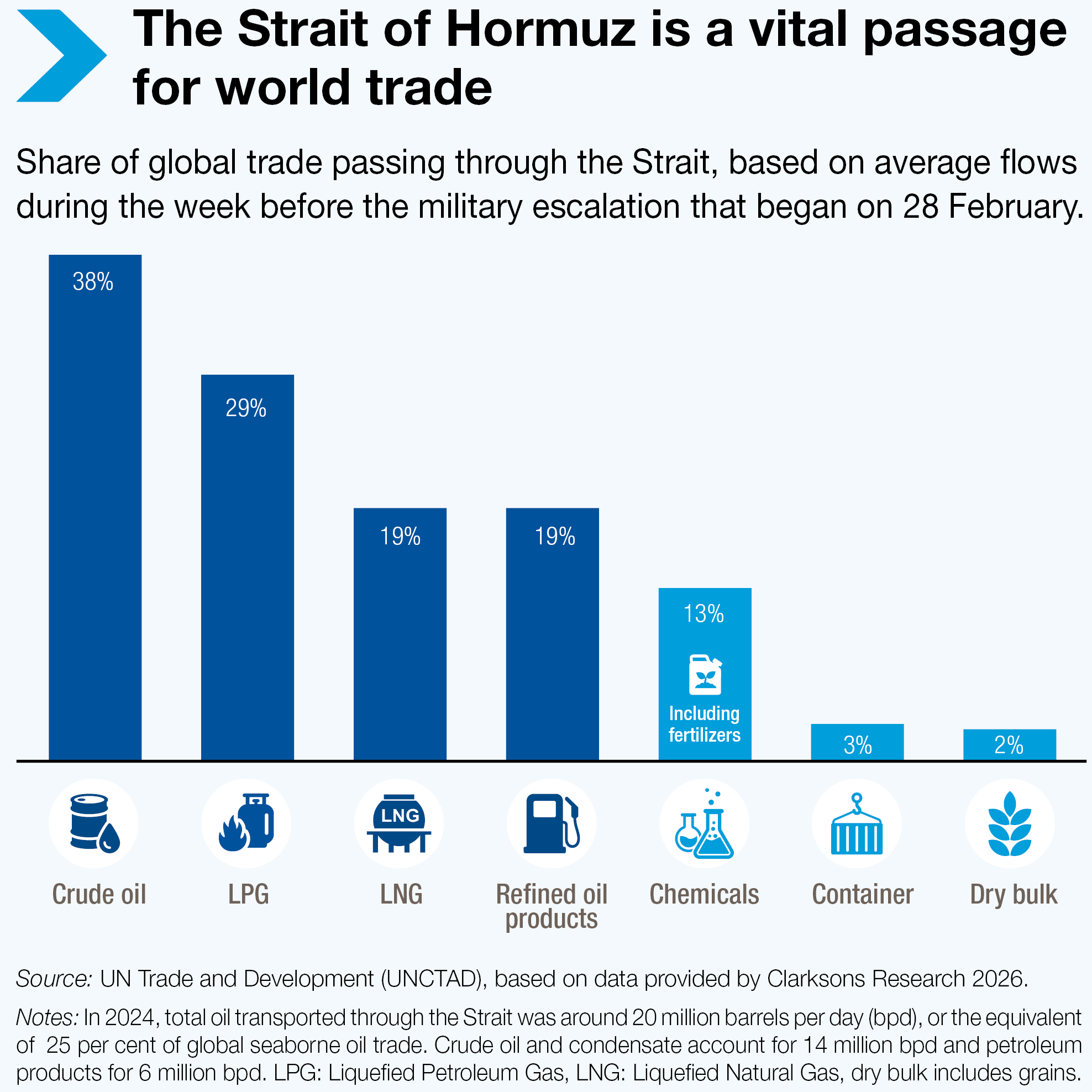

The Strait of Hormuz is a critical artery for global energy and fertiliser trade, carrying around a quarter of the world’s seaborne oil as well as significant volumes of liquefied natural gas and fertilisers. The scale of the disruption is therefore directly affecting both fuel and agricultural input markets.

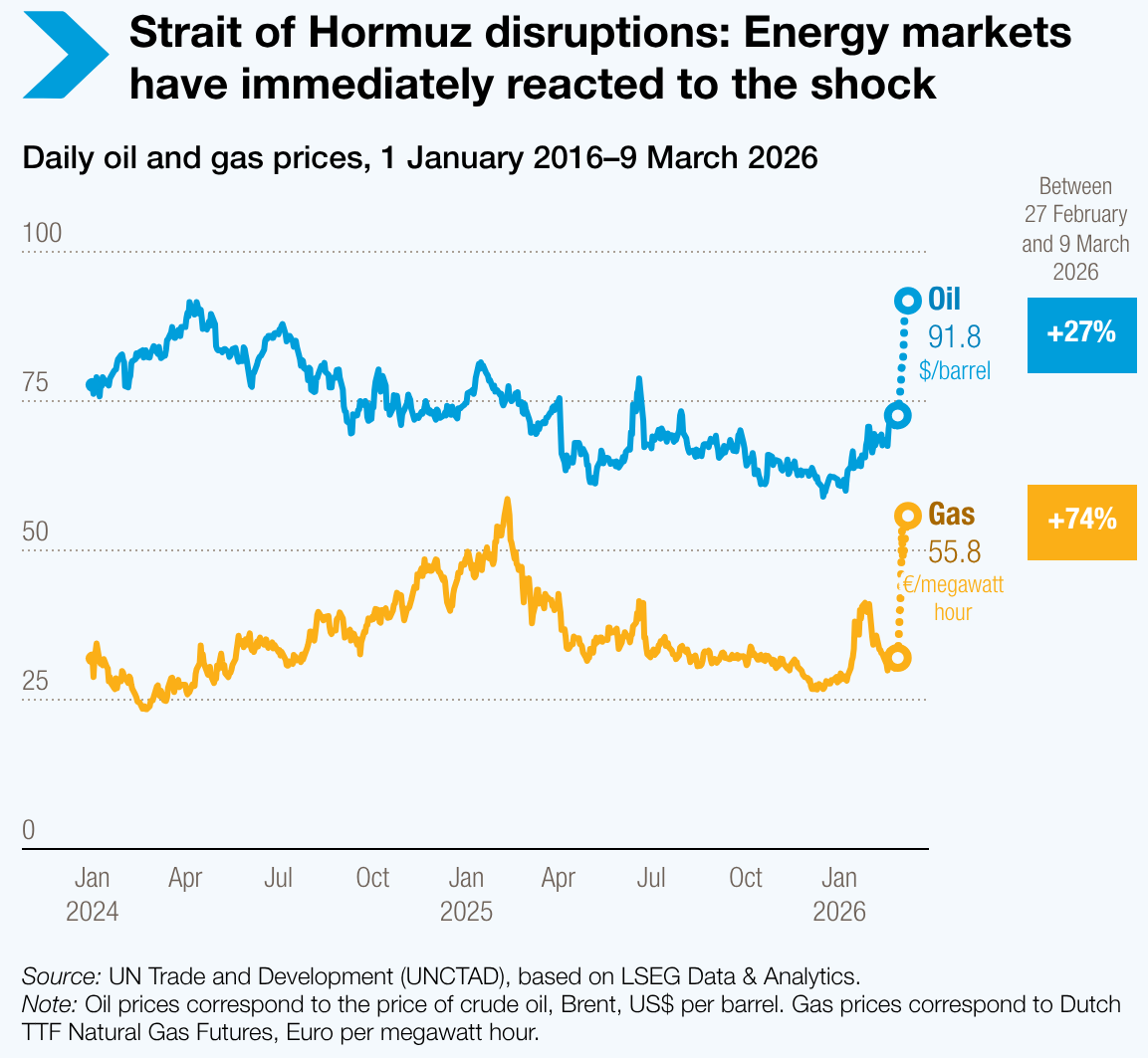

Energy markets have reacted immediately to the shock. Between February 27 and March 9, 2026, oil prices rose by about 27%, reaching approximately $91.8 per barrel, while natural gas prices increased by around 74%, with benchmark prices such as Dutch Title Transfer Facility futures rising to about €55.8 per megawatt hour, according to UNCTAD data based on LSEG Data and Analytics. Gas prices have surged sharply across both Europe and Asia, with Asian prices roughly doubling and Europe seeing similarly strong increases.

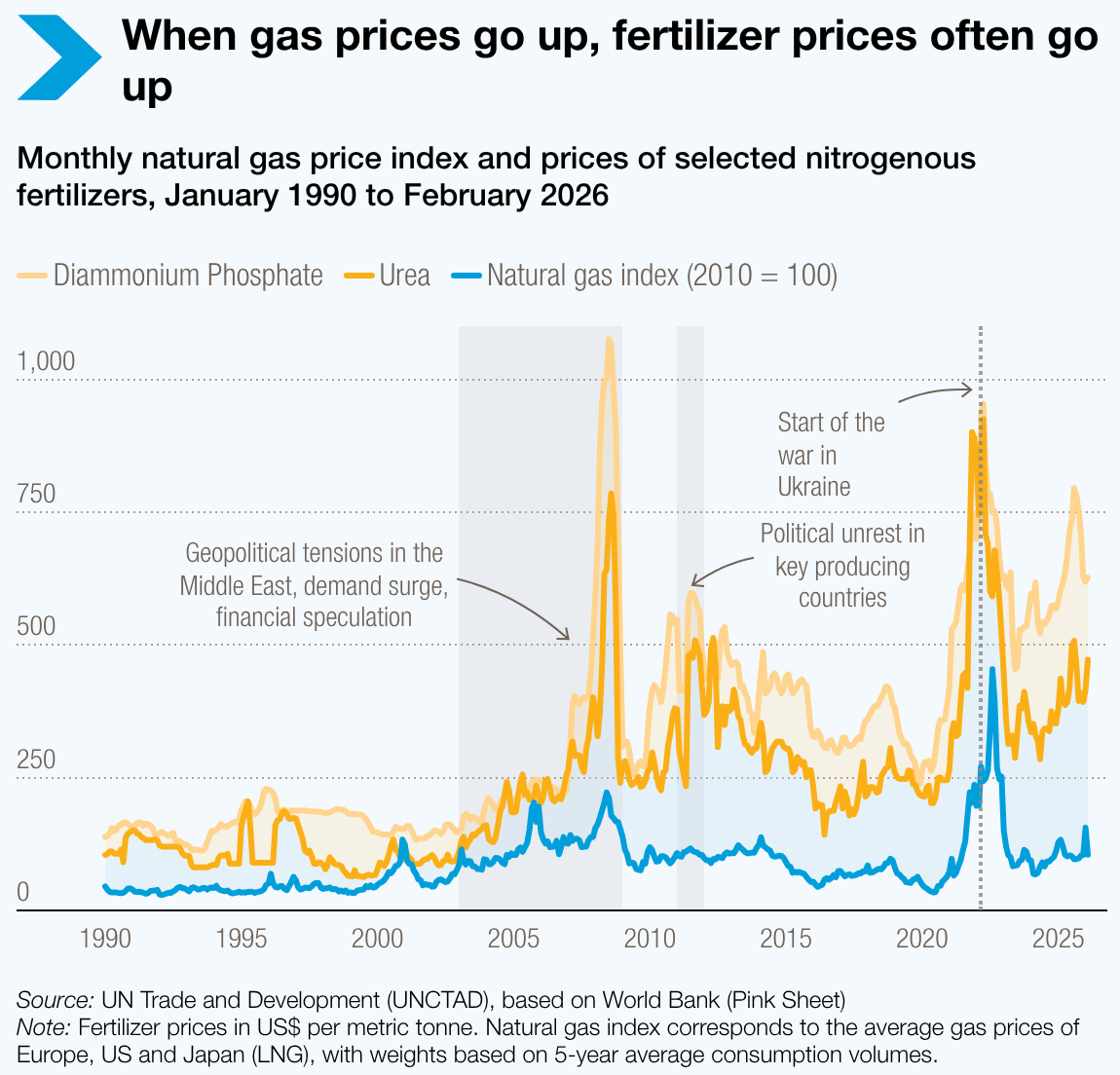

This surge is directly feeding into fertiliser markets. Natural gas is a key input in the production of nitrogen-based fertilisers such as urea and ammonia. Historical data show a strong correlation between gas prices and fertiliser prices, with increases in gas costs typically followed by rises in nitrogen fertiliser prices. Monthly price series from 1990 to February 2026, based on World Bank data, illustrate how geopolitical shocks, including the War in Ukraine and Middle East tensions, have previously driven simultaneous increases in energy and fertiliser prices.

The effects are already visible in current markets. Prices for nitrogen-based fertilisers have risen significantly, while phosphatic fertilisers such as diammonium phosphate have recorded smaller but noticeable increases. These developments mark a clear transmission of disruptions in energy and shipping into agricultural input markets, with implications for future food supply and trade.

The region’s importance extends beyond energy supply. It is also a major producer of key fertiliser inputs such as sulphur, used in phosphatic fertilisers, and a central hub for global fertiliser trade. Around one-third of global seaborne fertiliser volumes pass through the Strait, underscoring its strategic role in agricultural supply chains.

For major importing countries, particularly in Asia, disruptions to energy and fertiliser flows are closely interconnected. Reduced access to natural gas and rising costs are affecting fertiliser production, availability and trade flows simultaneously. The fertiliser trade is highly concentrated, increasing exposure to disruption. Countries in the region account for about 13% of global exports of nitrogen fertilisers and 9% of phosphate fertiliser nutrients.

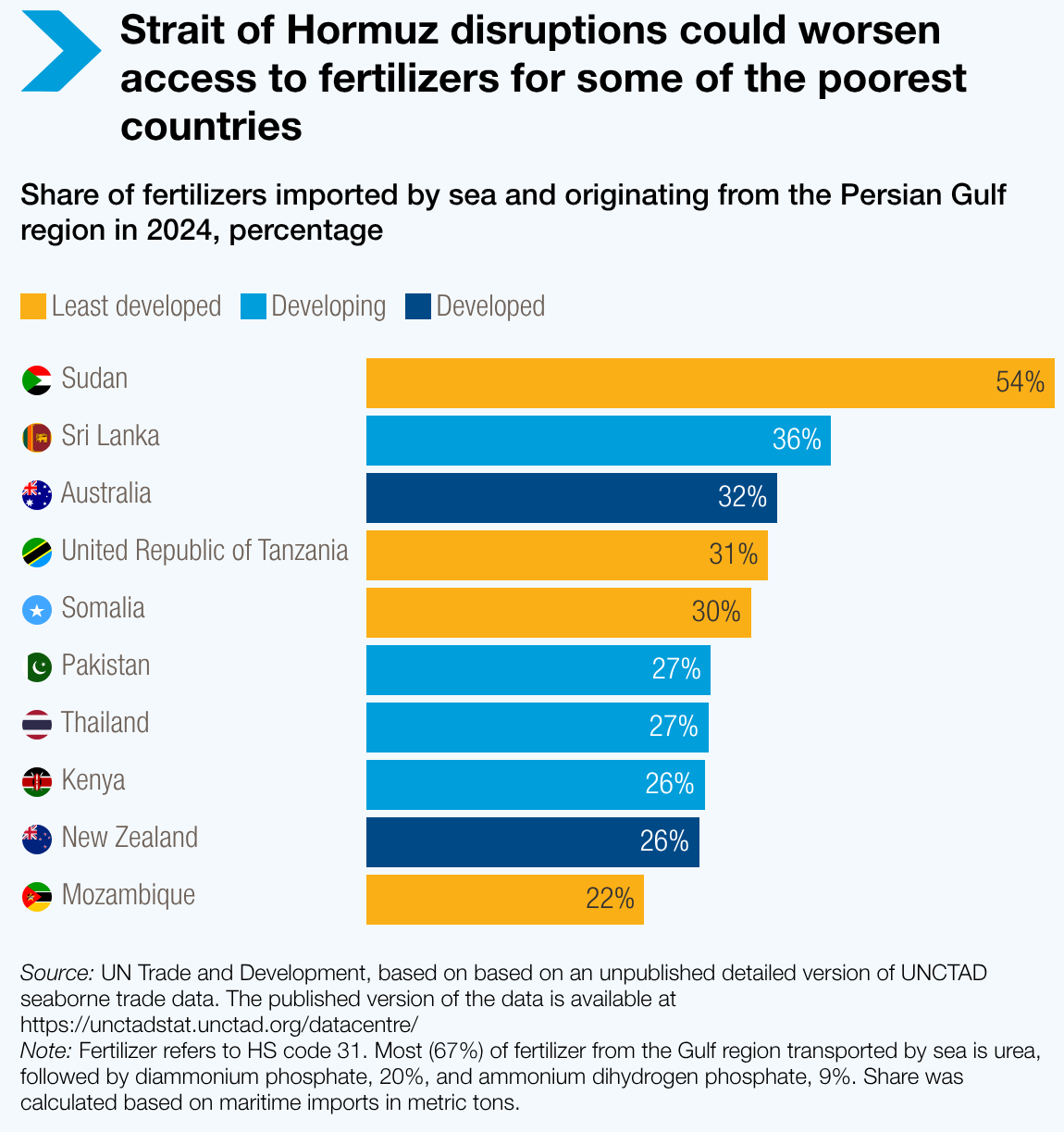

This dependence is especially pronounced in developing and least developed economies. UNCTAD data show that a significant share of fertilizer imports in countries such as Sudan (54%), Sri Lanka (36%), Australia (32%), the United Republic of Tanzania (31%), Somalia (30%), Pakistan (27%), Thailand (27%), Kenya (26%), New Zealand (26%) and Mozambique (22%) originates from the Gulf region. Most of this trade—about 67%—consists of urea, followed by diammonium phosphate at 20% and ammonium dihydrogen phosphate at 9%.

This reliance coincides with limited capacity to absorb price increases or secure alternative supplies. Many import-dependent economies face tight fiscal space, external imbalances and constrained access to finance, reducing their ability to respond to rising costs.

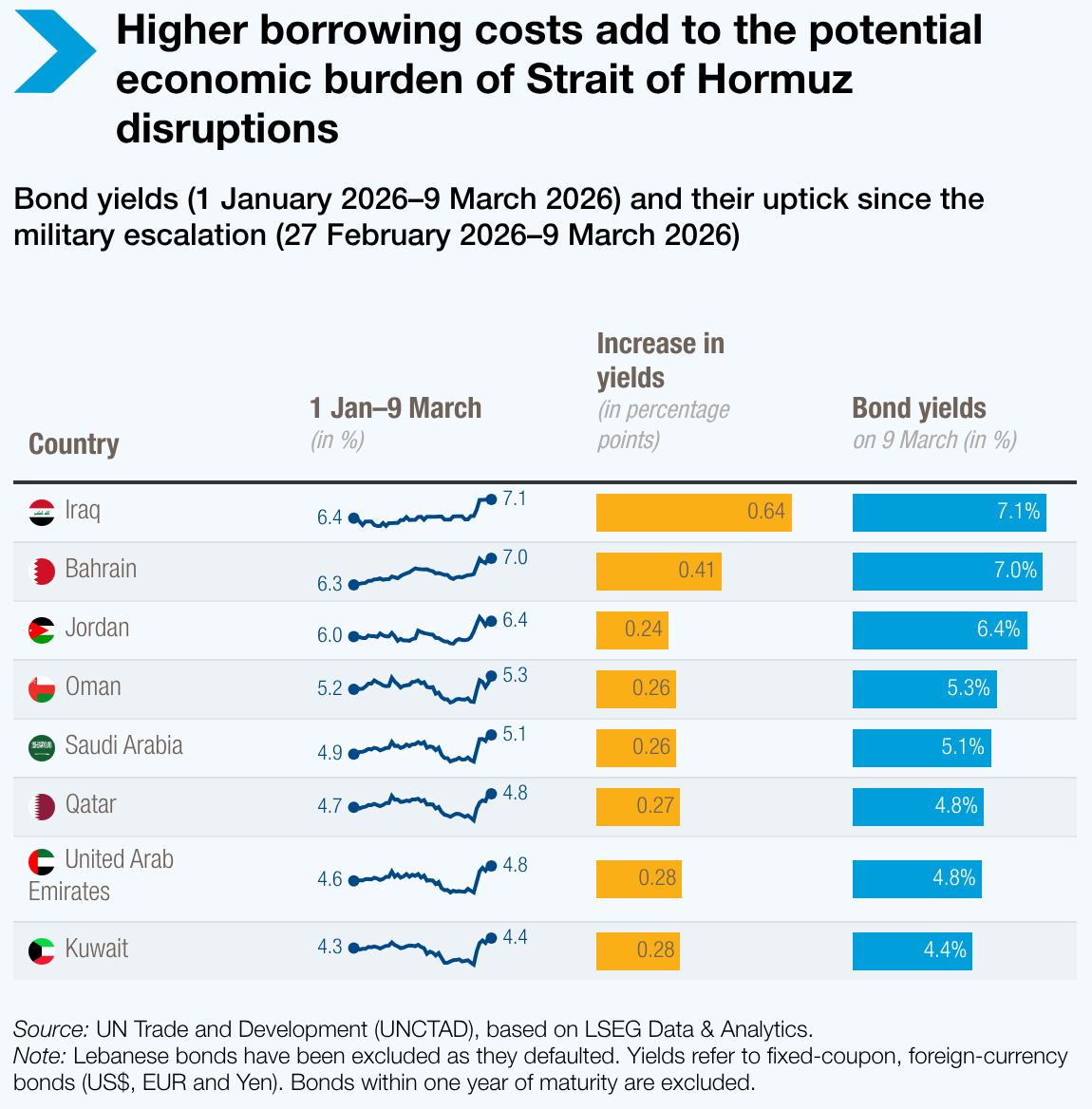

Financial conditions are tightening alongside supply disruptions. Bond yields have increased across several countries in the region between January 1 and March 9, 2026, with yields rising by about 0.24 to 0.64 percentage points. As of March 9, yields stood at around 7.1% for Iraq, 7.0% for Bahrain, 6.4% for Jordan, 5.3% for Oman, 5.1% for Saudi Arabia, 4.8% for Qatar and the United Arab Emirates, and 4.4% for Kuwait, reflecting higher borrowing costs and increased risk perceptions. Lebanese bonds were excluded due to default.

The disruption is also driving up transport and trade costs. Freight rates for oil tankers have risen by more than 90% since late February. Bunker fuel prices have nearly doubled, while war risk insurance premiums have surged several-fold, with some insurers withdrawing coverage altogether for vessels operating in the Persian Gulf. As a result, shipowners are being forced either to suspend transits or absorb sharply higher insurance costs, with premiums rising multiple times for each voyage.

These higher transport and insurance costs are feeding directly into fertiliser prices and, in turn, agricultural production and exports. Rising energy, fertiliser, and transport costs are increasing risks to food production, supply and prices, reinforcing the link between disruptions in energy markets and food systems.

While food insecurity is often associated with reliance on food imports, it is also closely tied to access to essential agricultural inputs. Disruptions to fertiliser supply therefore risk affecting production, yields and food availability, particularly in vulnerable regions.

Higher fertiliser costs influence planting decisions, including crop choice and total area planted, and affect input use and yields, with impacts materialising over time. For developing economies, these effects are compounded by structural constraints such as high debt burdens, limited fiscal space and rising borrowing costs. Limited access to finance further reduces producers’ ability to absorb rising costs.

The current situation illustrates how disruptions linked to the conflict are transmitting across interconnected commodity markets. Energy, fertilisers, and food are closely linked through production and trade systems, meaning constraints in one area can quickly affect others, with implications for food security, trade and development outcomes. The scale of these effects will depend on how long the disruptions persist. Current trends point to increasing pressure across commodity markets and supply chains, with the shock already moving from gas to grain.

– global bihari bureau